Alternative Minimum Tax Calculator to Help Exercise Your ISOs

- Rick Ruberg

- Feb 25

- 6 min read

The Alternative Minimum Tax (AMT) can really catch people off guard. It was created to ensure that those with higher incomes contribute their fair share, but the truth is, it can affect anyone who has significant capital gains, large deductions, or incentive stock options (ISOs).

If you understand how the AMT operates, you can plan ahead.

This means making smarter investment choices, timing your income more effectively, and knowing when deductions can actually help or hurt you.

I created this Alternative Minimum Tax Calculator. It’s a handy tool to quickly estimate your AMT liability, check if it applies to you, and start brainstorming strategies to lessen its impact before you file.

TL;DR: What this calculator answers

If you exercise ISOs and hold the shares past December 31, how much extra federal tax will you owe?

That number (the AMT hit) is the real cost of holding your shares for long-term capital gains treatment. The calculator shows it. The rest of this article explains what the number means and what you can do about it.

What Is the Alternative Minimum Tax (AMT)?

The AMT is a parallel tax system. You calculate your tax the normal way, then you calculate it a second time under AMT rules, and you pay the higher of the two.

AMT strips out a lot of the deductions and preferences the regular system gives you (the standard deduction, state and local taxes, and certain other items) and it treats specific events (like exercising ISOs) as immediate taxable income even when nothing is actually sold. It was originally aimed at a handful of wealthy taxpayers using aggressive deductions, but for years it drifted into middle-income territory until TCJA pulled most people back out.

What Changed Under the OBBBA

The One Big Beautiful Bill Act (OBBBA), signed in July 2025, made the higher TCJA exemption amounts permanent, but it also tightened the phaseout rules starting in 2026. Two things to know:

Exemption amounts are permanent and indexed for inflation. The generous TCJA-level exemptions are not going away.

Phaseout thresholds dropped significantly and phase out twice as fast. For 2026, the exemption begins phasing out at $500,000 (single) and $1,000,000 (MFJ) — down from $626,350 / $1,252,700 in 2025. And the phaseout rate doubled from 25% to 50%.

If you're a high earner exercising ISOs, 2026 is a harder AMT environment than 2025 was. If you're middle-income, nothing really changed for you.

When Does the AMT Kick In?

AMT generally kicks in when your AMT taxable income exceeds the AMT exemption amount.

This often occurs due to:

Exercising Incentive Stock Options (ISOs) and holding the stock through year-end.

Having large state and local tax (SALT) deductions.

Claiming significant miscellaneous itemized deductions.

Having depreciation differences or tax-exempt interest from private activity bonds.

2026 AMT Exemption Amounts and Phaseouts

Filing Status | 2026 Exemption | Phaseout Begins |

Single / HoH | $90,100 | $500,000 |

Married Filing Jointly | $140,200 | $1,000,000 |

Married Filing Separately | $70,100 | $500,000 |

Complete phaseout: the exemption is fully eliminated once AMTI reaches $680,200 (single) or $1,280,400 (MFJ). Above those levels, every dollar of AMTI is taxed at AMT rates.

AMT rate brackets for 2026: 26% on the first $244,500 of taxable excess ($122,250 if MFS); 28% on anything above that. These rates apply to all filing statuses, the split is not different for single vs. joint filers.

Calculate Alternative Minimum Tax

The steps to calculate AMT are:

Start with your taxable income (from Form 1040, before the AMT calculation).

Add back “AMT preferences and adjustments”, like:

ISO bargain element (FMV – strike price)

Disallowed state/local tax deductions

Miscellaneous itemized deductions

This gives you AMTI (Alternative Minimum Taxable Income).

Subtract the AMT exemption.

Apply AMT tax rates:

26% on the first portion (up to $244,500 for joint filers in 2025)

28% on the amount above that

Compare the AMT to your regular tax. If AMT is higher, you owe the difference on top of your regular tax.

...Enter your numbers, see the hit, and decide whether to exercise, hold, or split the difference.

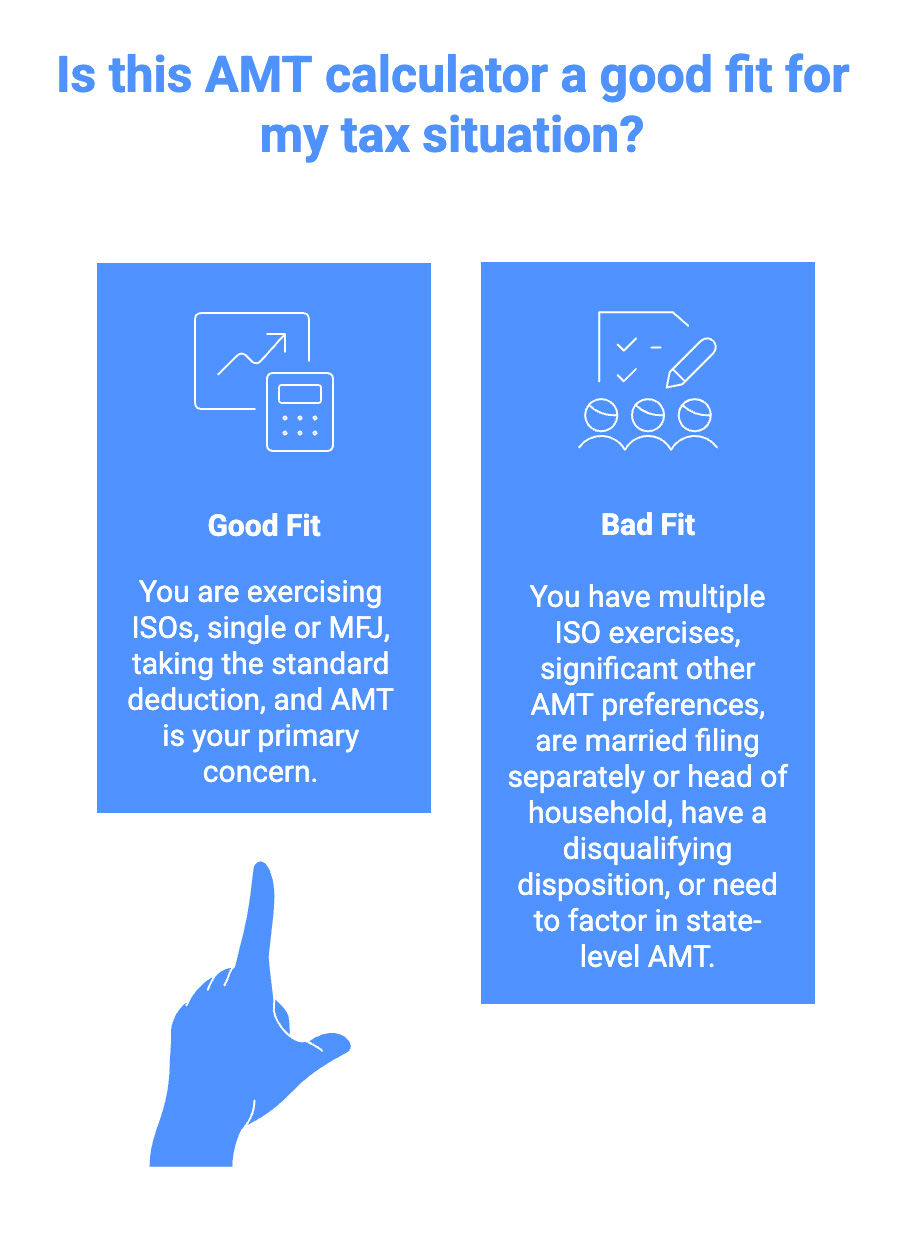

*This calculator uses simplified assumptions and does not account for State taxes, multiple ISO exercises, or all filing statuses.

AMT Calculator Assumptions:

Applies the standard deduction.

Assumes this ISO exercise is the only AMT preference item.

Excludes State taxes.

Assumes no other ISO exercises or AMT preference items during the year.

Treats income as ordinary income (not long-term capital gains).

Filing status options are limited to Single or Married Filing Jointly (no support for Married Filing Separately or Head of Household).

How to Read Your Calculator Results

The calculator output answers one specific question... based on the ISO exercise you're modeling, how much extra federal tax will you owe compared to what you'd pay without the exercise? That difference is your AMT hit.

A few things worth knowing about that number:

The AMT you pay on an ISO exercise isn't necessarily gone forever

When AMT is triggered by an ISO exercise, you generally build up a minimum tax credit (Form 8801). In future years, when your regular tax exceeds your tentative minimum tax, you can use that credit to reduce your regular tax bill. You may eventually get some or all of the AMT back — it just might take years. This is why a lot of advisors frame ISO AMT as a "prepayment" rather than a permanent cost. It doesn't always work out cleanly, but it's a critical nuance most ISO holders miss.

There's an "AMT break-even" point

For any given income level, there's a maximum ISO bargain element you can realize without triggering AMT. Below that line, exercising is essentially free from an AMT standpoint. Above it, every additional dollar of bargain element costs you 26-28 cents in AMT (more if you're in the phaseout zone). Play with the calculator — try increasing the bargain element in steps and watch when the AMT number goes from zero to something. That transition point is your break-even, and it's the cleanest way to size an exercise.

The AMT hit is the price of long-term capital gains treatment

The reason people hold ISO shares past year-end is to start the clock on long-term capital gains — a qualifying disposition requires holding at least one year from exercise and two years from grant. The AMT number the calculator shows you is, effectively, the price you're paying to get that LTCG treatment. Whether it's worth it depends on your spread between ordinary and LTCG rates, your conviction in the stock, and your cash position.

Common ISO Planning Moves

A few strategies worth discussing with your tax advisor:

Exercise early in the year, then watch the stock.

If it tanks by December, you can do a disqualifying disposition (sell before year-end) and avoid the AMT hit entirely, you'll pay ordinary income on the reduced spread instead of AMT on the higher exercise-date spread.

Exercise up to your AMT break-even each year.

Rather than doing one big exercise, stagger smaller exercises over multiple years that each stop just short of triggering AMT.

Exercise in a low-income year.

A sabbatical, job change, or pre-IPO year with little W-2 income is the cheapest time to exercise, your break-even point is much higher.

Exercise and immediately sell (cashless / same-day).

This is a disqualifying disposition. You lose LTCG treatment, but you avoid AMT entirely and get the cash. Sometimes the right call, especially if you don't have cash to cover the AMT bill.

Bottom Line

For most taxpayers, AMT is a insignificant. For ISO holders sitting on a large paper gain, it's the single biggest variable in the exercise vs. hold decision. The rule changes under OBBBA tightened the rules for high earners specifically, so if you're near those phaseout thresholds, modeling matters more than it did in the past.

Run the numbers, look at your break-even, and then talk to your tax advisor before pulling the trigger.

Disclaimer:

This calculator is provided for informational purposes only and should not be relied upon as legal, tax, or financial advice. 100bonusdepreciation.com does not provide professional advisory services, and this tool is not a substitute for consultation with a qualified advisor who understands your individual circumstances. By using this calculator, you acknowledge and agree that any decisions or actions you take are at your own risk. 100bonusdepreciation.com makes no guarantees regarding the accuracy, applicability, or completeness of the results, and we are not liable for any loss or damages arising from its use or reliance. This calculator is provided “as is,” without any express or implied warranties, including but not limited to warranties of merchantability, fitness for a particular purpose, satisfactory quality, title, or non-infringement. Some jurisdictions do not allow the exclusion of implied warranties, so certain limitations may not apply to you.

Comments