Tax Brackets in 2026: What Real Estate Investors Need to Know

- Rick Ruberg

- Apr 13

- 4 min read

The IRS has released its inflation-adjusted tax parameters for the 2026 tax year, and for the first time, these numbers reflect the permanent tax structure established by the One Big Beautiful Bill Act (OBBBA). Here's what changed in the tax brackets and what it means for your planning.

What's Different in 2026

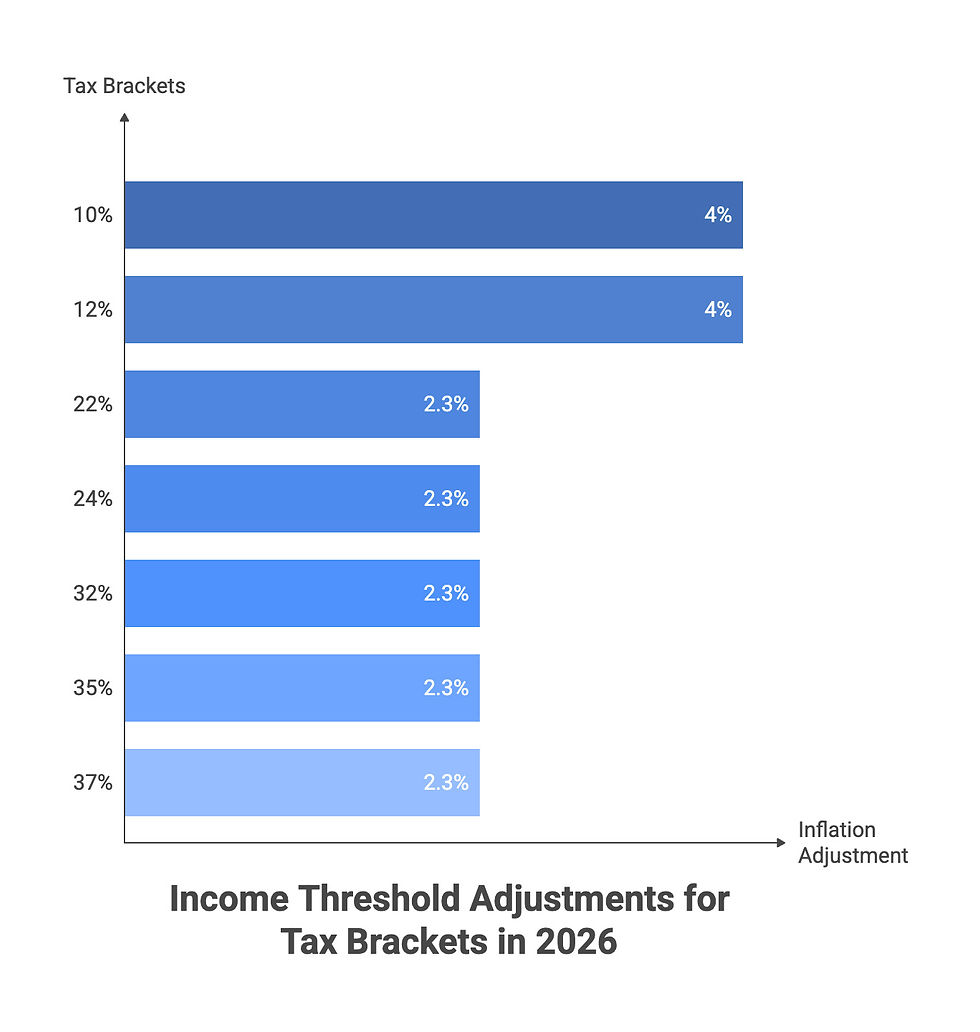

The tax rates themselves haven't changed... you're still looking at 10%, 12%, 22%, 24%, 32%, 35%, and 37%. What shifted are the income thresholds, and not uniformly.

The OBBBA gave the bottom two brackets (10% and 12%) a larger inflation adjustment of roughly 4%, while the upper five brackets received the standard ~2.3% bump. The result is a slightly wider runway before you cross into the 22% bracket and above.

Standard Deduction Increases

The standard deduction continues to climb, providing a larger shield against taxable income before you even get to bracket math.

Filing Status | 2025 | 2026 | Change |

Single | $15,750 | $16,100 | +$350 |

Married Filing Jointly | $31,500 | $32,200 | +$700 |

Head of Household | $23,625 | $24,150 | +$525 |

For real estate investors, the standard deduction is often a non-factor since mortgage interest, property taxes, and other itemized deductions typically exceed it. But for those in transition years (perhaps between properties or restructuring holdings) knowing these thresholds matters.

Federal Income Tax Brackets for 2026

Single Filers

Taxable Income | Tax Rate |

$12,400 or less | 10% |

$12,401 to $50,400 | 12% |

$50,401 to $105,700 | 22% |

$105,701 to $201,775 | 24% |

$201,776 to $256,225 | 32% |

$256,226 to $640,600 | 35% |

$640,601 and above | 37% |

Married Filing Jointly

Taxable Income | Tax Rate |

$24,800 or less | 10% |

$24,801 to $100,800 | 12% |

$100,801 to $211,400 | 22% |

$211,401 to $403,550 | 24% |

$403,551 to $512,450 | 32% |

$512,451 to $768,700 | 35% |

$768,701 and above | 37% |

Head of Household

Taxable Income | Tax Rate |

$17,700 or less | 10% |

$17,701 to $67,450 | 12% |

$67,451 to $105,700 | 22% |

$105,701 to $201,775 | 24% |

$201,776 to $256,200 | 32% |

$256,201 to $640,600 | 35% |

$640,601 and above | 37% |

Source: IRS Revenue Procedure 2025-32

The AMT Changes Worth Watching

The Alternative Minimum Tax (AMT) exemption amounts increased modestly, $90,100 for single filers and $140,200 for married couples filing jointly, up from $88,100 and $137,000 in 2025.

The OBBBA reset the AMT phaseout thresholds significantly lower... down to $500,000 for single filers and $1,000,000 for joint filers (compared to $625,350 and $1,252,700 in 2025). It also accelerated the phaseout rate from 25 cents to 50 cents per dollar of income above those thresholds.

What does that mean in practice? High-income investors who were previously clearing the AMT exemption phaseout may now lose their exemption faster. If you're a real estate professional with significant rental income or capital gains layered on top of W-2 income, this is worth modeling with your CPA.

New Senior Deduction

The OBBBA introduced a brand-new deduction for taxpayers aged 65 and older, $6,000 per qualifying taxpayer (up to $12,000 for married couples), available whether you itemize or take the standard deduction. This phases out at 6% of income above $75,000 (single) or $150,000 (joint).

This stacks on top of the existing additional standard deduction for seniors ($2,050 for single filers, $1,650 per qualifying spouse for joint filers). For older investors drawing rental income or managing a portfolio of depreciated properties, it's a meaningful reduction.

Section 199A Made Permanent

The 20% Qualified Business Income (QBI) deduction for pass-through entities is now permanent under the OBBBA. For 2026, the income thresholds where deduction limitations begin to phase in are $201,775 (single) and $403,500 (joint), with the phaseout range widened to $75,000 and $150,000 respectively.

If you own rental properties through an LLC or S-corp, this deduction remains one of the most valuable line items on your return, and knowing it's permanent changes the calculus on entity structuring decisions that used to carry a sunset risk.

Other Notable Adjustments for 2026

Child Tax Credit:

The maximum CTC is $2,200 per qualifying child (increased from $2,000 by the OBBBA), now indexed for inflation going forward. The refundable portion remains at $1,700.

Earned Income Tax Credit:

The maximum EITC rises to $8,231 for families with three or more qualifying children.

Estate Tax Exclusion:

Increased to $15 million per person, up from $13.99 million in 2025, and made permanent. For investors with significant real estate holdings, this removes the urgency that surrounded estate planning under the old sunset timeline.

Gift Tax Exclusion:

Remains at $19,000 per recipient.

What This Means for Tax Planning

The permanence of the TCJA structure under the OBBBA is arguably the biggest development here, bigger than any individual bracket shift. For years, real estate investors and their advisors planned around a potential 2026 cliff where rates could revert to pre-TCJA levels. That uncertainty is gone.

With brackets now locked in and indexed for inflation, the planning focus shifts to optimizing within a known framework: timing income recognition, accelerating deductions through strategies like cost segregation and bonus depreciation, and structuring pass-through entities to maximize the 199A deduction.

Work with a qualified tax professional to model how these 2026 changes interact with your specific portfolio. The bracket shifts are modest, but the structural permanence opens up multi-year planning strategies that weren't practical under sunset risk.

Related: 100% bonus depreciation is back - permanently. Read our full breakdown →

Comments